Downtown is the global music publishing admin for Peso Pluma (pictured) and his Double P Records label. Downtown's publishing division is now generating $200 million in gross revenues annually, according to a Billboard report

“Last Christmas, I gave you my heart. But the very next…” *RECORD SUDDENLY SCRATCHES*

We interrupt this cozy festive tableau to inform you that Universal Music Group/Virgin Music Group has agreed a $775 million deal to buy services giant Downtown Music. Now, please, return to your celebrations.

Did UMG’s big announcement yesterday (December 16) feel this way to anyone else?

Just us?

The timing may, of course, have been purely coincidental.

Deals of this size are, by their very nature, complicated, and we’re used to seeing them forced over the line just in time for the Holidays. (It’s presumably deemed gauche for C-suite execs to still be conducting one’s M&A business on the beaches of St. Barts in early January.)

Yet there’s also that… other possibility.

Universal Music Group might have been keen to squeak out the Downtown acquisition announcement just as we were all starting to get a little merry and a little sherry(‘d) – thus limiting the loudness of the inevitable backlash from certain businesses.

That backlash arrived today (December 17) regardless, from predictable sources.

Echoing the sentiments of IMPALA, Martin Mills, founder of Beggars Group said: “This is another step on the road of UMG’s pretence to be the independents’ fairy godmother. But there’s a wolf under that cape.”

He’s an indie maverick, so Mills is permitted to play a little fast and loose with his fairytales (only a badass Fairy Godmother would wear a cape!). But his point is clear: beware the ‘indie’ distribution expansion of the biggest of the ‘Big Three’.

Beyond indie-sector outrage (and the attempted stoking of regulatory scrutiny), the proposed Downtown takeover – which UMG expects to complete in the latter half of 2025 – offers a number of other interesting elements.

1) Downtown Music Holdings is/is about to become… a unicorn 🦄

If UMG/Virgin Music Group’s proposed takeover of Downtown Music is approved, it will see a number of the latter company’s subsidiaries become part of the major’s setup. These include:

Premium recorded music services division, Downtown Artist & Label Services;

A prestige publishing admin company (Downtown Music Publishing, including Sheer in Africa), plus a pub admin platform for DIY-level writers, Songtrust;

Royalty processing and analytics platform, Curve.

What UMGisn’t buying in this deal, however, is any copyrights.

Since 2021, Downtown has been a ‘pure’ services business, i.e. working with thousands of artists and songwriters who retain ownership of their musical IP.

“Downtown founder Justin Kalifowitz and his team built a company worth some $1.175 billion since launching in 2007.”

That’s because, in 2021, Downtown sold its portfolio of owned songs (covering some 145,000 copyrights) to Concord for approximately $400 million.

That $400 million, plus the $775 million that Universal/Virgin Music Group is now willing to pay for Downtown Music (the services company) gives us Downtown Music Holdings’ true exit value: $1.175 billion.

Yup: Since launching Downtown Music Holdings in 2007, company founder Justin Kalifowitz and his team have officially built a shiny unicorn.

Not bad.

Beto Vega

2) This is partly about recorded music market share… especially in Latin America

Earlier this year I wrote a piece for MBW+ subscribers outlining the growing distribution market share of the independent recorded music sector vs. the ‘Big Three’ majors.

The central data point in that piece came from Luminate, the standard-bearer market monitor for music consumption in the US and globally.

It showed that indie distribution growth (at the expense of major music companies) wasn’t just happening in the ‘long tail’ – it was impacting bigger artists, too.

Luminate’s midyear stats showed that indie-distributed tracks claimed one in every ten tracks (9.9%) that had been streamed over 500 million times in the US in H1 2024 (see below).

That 9.9% figure was up significantly, from 7.1%, in the same period of the prior year.

In other words, the major music companies had lost close to 3% US market share of tracks streamed over 500 million times (per half-year) in the space of just 12 months.

A slide from Luminate’s 2024 Midyear report, showing distribution market share changes in the US in H1 2024 vs. H2 2023 segmented by total on-demand audio streams of tracks in each period

This is far from only being a US phenomenon, of course.

Midia Researchstats show that the global distribution share of non-major music companies (including labels distributed by indies plus self-releasing artists) hit 36.7% in 2023 ($12.9bn vs. total revenues of $35.1bn).

That indie global market share percentage has steadily grown year-on-year over the past decade – at the expense of the majors.

An acquisition of Downtown’s ‘Artist & Label Services’ division would give Virgin Music Group a big boost in one region in particular.

Downtown’s A&LS division has seen particular success in Latin America, with a specific drive in the Musica Mexicana market.

Today, A&LS distributes Musica Mexicana artists including Beto Vega, plus labels including Alzada Music (home to the late Lefty SM, plus Yoss Bones), Delux Music Group (Daniel Garcia and Erick B) and Master Q (Los Tucanes de Tijuana).

In March, Downtown’s A&LS division said it was generating an average of 200 million streams in the Musica Mexicana genre per day – up 65% YoY.

“there’s plenty of room to grow in Latin America… We like our prospects there.”

JT Myers, Virgin Music Group, speaking last year

(Downtown’s expertise in Musica Mexicana also expands to its publishing division, which re-upped with long-time client Peso Pluma and his Double P label in August.)

“Kudos to The Orchard for seeing something before anybody else did and, yes, we’ve got catching up to do,” said Myers.

“But there’s plenty of room to grow in Latin America and we’ve made great progress. We like our prospects there.”

Credit: Shutterstock3) Universal will have to think hard how to merge Downtown into Virgin… while still growing its own margin

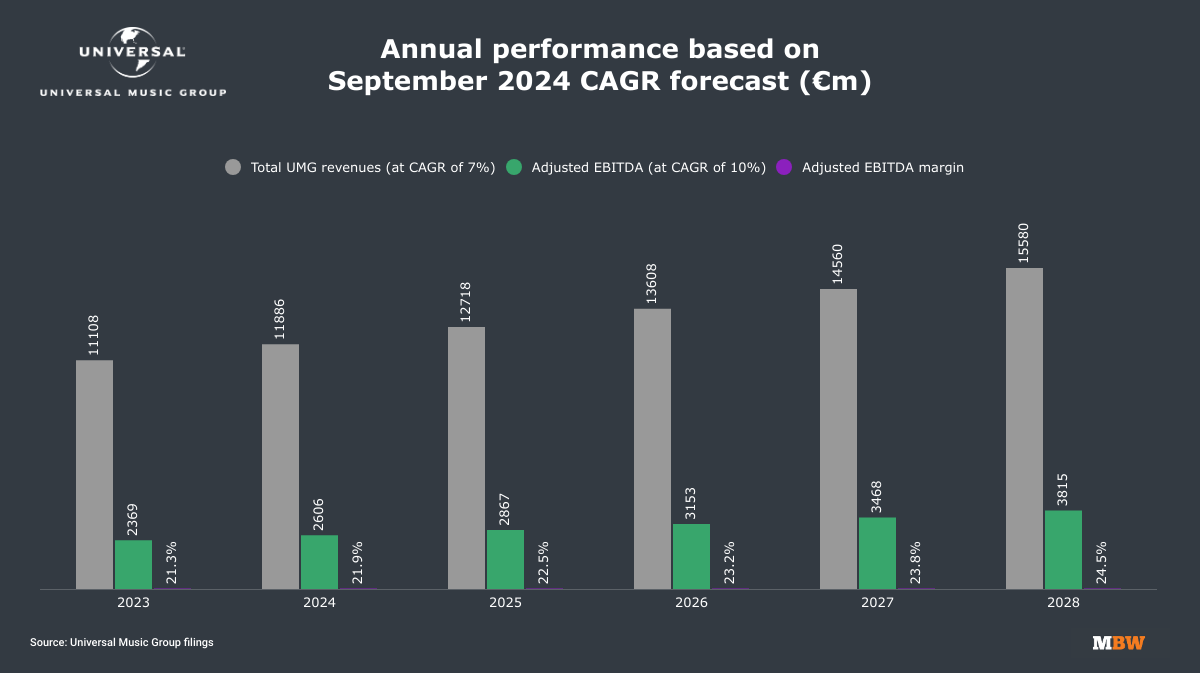

Universal Music Group previously told investors that it’s targeting an adjusted EBITDA margin of 25% in the next 2-3 years.

In September, that changed: UMG dropped this mid-term EBITDA guidance for something new – a forecast of an average 10%+ annual CAGR for its adjusted EBITDA through FY 2028 at constant currency.

MBW has run the sums on that average annual 10%+ CAGR forecast (and a separate CAGR guidance for revenue, also given in September).

It suggests UMG’s adjusted EBITA margin should land somewhere around 24.5% by the end of 2028.

(A cost-saving program at UMG is underway and is continually helping to improve the firm’s adjusted EBITDA figure.)

To be clear, the adjusted CAGR forecast given by UMG in September isorganic – i.e. discounting any M&A activity that may take place along the journey to FY2028.

That being true…

The addition of Downtown Music will most certainly drive significant market share gains for UMG, both in recorded music distribution plus, potentially, publishing (see pt.2 above).

But what might it do to Universal’s overall margin profile?

Downtown, like most services businesses, is a single-digit margin company.

According to sources talking to Billboard, Downtown’s latest annual gross revenues stood at around $900 million, with net revenues (i.e. after copyright-holding clients have been paid) of $130 million.

Finally, after Downtown’s operating costs are taken into account, annual EBITDA weighs in at around $40 million.

Can Universal, via Virgin Music Group, find enough synergies to significantly raise Downtown’s profitability profile?

Or might the Downtown acquisition see UMG adjust its own (inorganic) EBITDA margin target to accommodate the benefits of its new acquisition?

(Relevant: Downtown just told Billboard that its publishing division will generate over $200 million in gross revenue in 2024, up 40% YoY.)

On the flip side, could Downtown’s addition to Universal’s Virgin Music Group (VMG) actually bring new margin-accretive opportunities?

For example: how many current VMG clients around the globe could be ‘upsold’ into using Curve Royalty Systems, an acclaimed music royalty processing/management platform that was acquired by Downtown last year?

Similarly, Downtown brings a new opportunity for VMG in FUGA.

The self-proclaimed ‘largest full-service B2B music distributor in the world’, FUGA may improve VMG’s digital supply chain efficiency and attract new clients into the VMG universe.

FUGAcurrently works with over 1,000 prestige indie labels globally, including the likes of Beggars Group, Domino, Epitaph, and Armada.

Its ingestion into VMG may represent a useful ‘funnel’ via which Virgin starts an arm’s length relationship with a previously untouched indie client base.

Conversely, if said indie clients are determined to leave the UMG/Downtown world (see Martin Mills’ comments RE: UMG/Downtown) it could also represent an opportunity for FUGA rivals, including SESAC-owned AudioSalad.

UMG’s adjusted EBITDA margin stood at 21.4% in FY2023

4) What will become of CD Baby?

So, to sum up much of the above: profit margin challenges aside, an acquisition of Downtown offers Virgin Music Group (VMG) and, potentially (?) Universal Music Publishing Group (UMPG), an obvious opportunity to grow market share… while also enhancing VMG’s service offering.

Yet there’s one component of Downtown Music that might not fit so well into the Virgin/Universal setup: CD Baby.

The DIY distribution company, a rival to TuneCore and DistroKid, was servicing more than 2 million self-releasing ‘creators’ as of November last year, representing over 20 million tracks.

Regular readers of MBW will know that UMG boss, Sir Lucian Grainge, hasn’t exactly shown himself to be the biggest fan of DIY distribution platforms to date.

For one thing, Grainge has spearheaded ‘artist-centric’ changes at streaming services that – to give one example – now prevent indie tracks from earning any royalties until they hit 1,000 streams annually on Spotify.

The upshot: ‘artist-centric’ models shift royalty micro-payments away from artists with a mere handful of listeners, and towards artists with larger fanbases.

“Those groups who have expressed a concern about ‘artist-centric’ [streaming royalties] are unsurprisingly those whose business model is based on being merchants of garbage. Sorry, I can’t really think of another word for content that no one actually wants to listen to.”

Sir Lucian Grainge on certain DIY platforms, October 2023

Summing up his general view of low-streaming DIY music, Grainge said in October 2023 that those companies objecting to ‘artist-centric’ changes at streaming platforms were “unsurprisingly those whose business model is based on beingmerchants of garbage”.

Virgin Music Group heads JT Myers and Nat Pastor then told MBW in Q4 last year that they had “no intention” of entering the DIY distribution arena for similar reasons.

Said Myers: “Major labels used to get criticized for ‘throwing a bunch of s–t against the wall and seeing what sticks’ [as they would sign many artists and only a few would be successful].

“Well the [DIY aggregation world] casts the net even wider. It’s not why we got into the music business.”

CD Baby, then, is an odd cultural fit at UMG… and buying it definitely won’t do much to increase Universal’s EBITDA margin.

Yet Downtown itself saw significant value in CD Baby, paying around $200 million to acquire it via parent AVL Digital in 2019.

All of which taken into account… if I were a betting man I’d wager that, should regulators approve UMG’s acquisition of Downtown next year, we’ll see Universal then look to offload CD Baby to: (a) a private equity buyer, or (b) a company proud to specialize in the world of self-uploading amateur artists.

Who knows? Maybe that company could be Believe… once the small matter of UMG’s $500 million lawsuit against the French firm is done and dusted, anyway.Music Business Worldwide