Apple has enough spare money to buy the entire music business. Just like that.

According to its latest financial results, Apple Inc currently has a fictional-sounding cash position of $246.1bn – 94% of which ($231.3bn) is held outside the US.

Judging by market caps and public valuations, Apple could snap up Vivendi ($23bn), Sony Corp ($38bn), Live Nation ($6bn), Pandora ($3bn) and Spotify ($8bn) for less than a third of its current savings – and still leave change on the table.

One of the few companies Apple couldn’t hypothetically afford for that kind of money is… Apple, whose current market cap ($624bn) makes it worth approximately 7,700% more than Daniel Ek‘s IPO-chasing green machine, Spotify.

So what’s Tim Cook going to do with this mountain of money?

That’s a less important question right now than what he’s willing to do with it – especially in the wake of AT&T’s historic $85bn takeover bid for TV and movie content giant Time Warner.

Lest we forget that Apple was itself closely linked with a buyout of HBO owner Time Warner towards the end of last year.

Is it about to make a major content acquisition of its own?

That was the question put to the company’s CEO Tim Cook in Apple’s Q1 earnings call on Tuesday (Jan 31) – and his answer will have set tongues wagging across myriad entertainment industries.

After acknowledging that he was hopeful Donald Trump’s administration may create tax conditions in the US which would make the ‘repatriation’ of Apple’s cash mountain more appealing, Cook said:

“What we would do with [this money], let’s wait and see exactly what it is… [but] we are always looking at acquisitions. We acquired 15 to 20 companies per year for the last four years.

“We are always looking at acquisitions. We look for companies of all sizes.”

Tim Cook, Apple

“And we look for companies of all sizes – there’s not a size that we would not do based on just the size of it. It’s more about the strategic value of it.”

When you can afford to buy almost everyone, it makes sense to consider the advantages of buying anyone.

Perhaps that’s why Apple has also been recently linked with swooping for $60bn-valued Netflix.

Depending on Cook’s appetite to take on the TV and movie market, that would potentially offer plenty of ‘strategic value’.

![]()

Because Tim Cook’s openness to consider a major content acquisition comes hand-in-hand with Apple’s increasing focus on its ‘Services’ segment – which includes Apple Music, Apple Pay and the App Store.

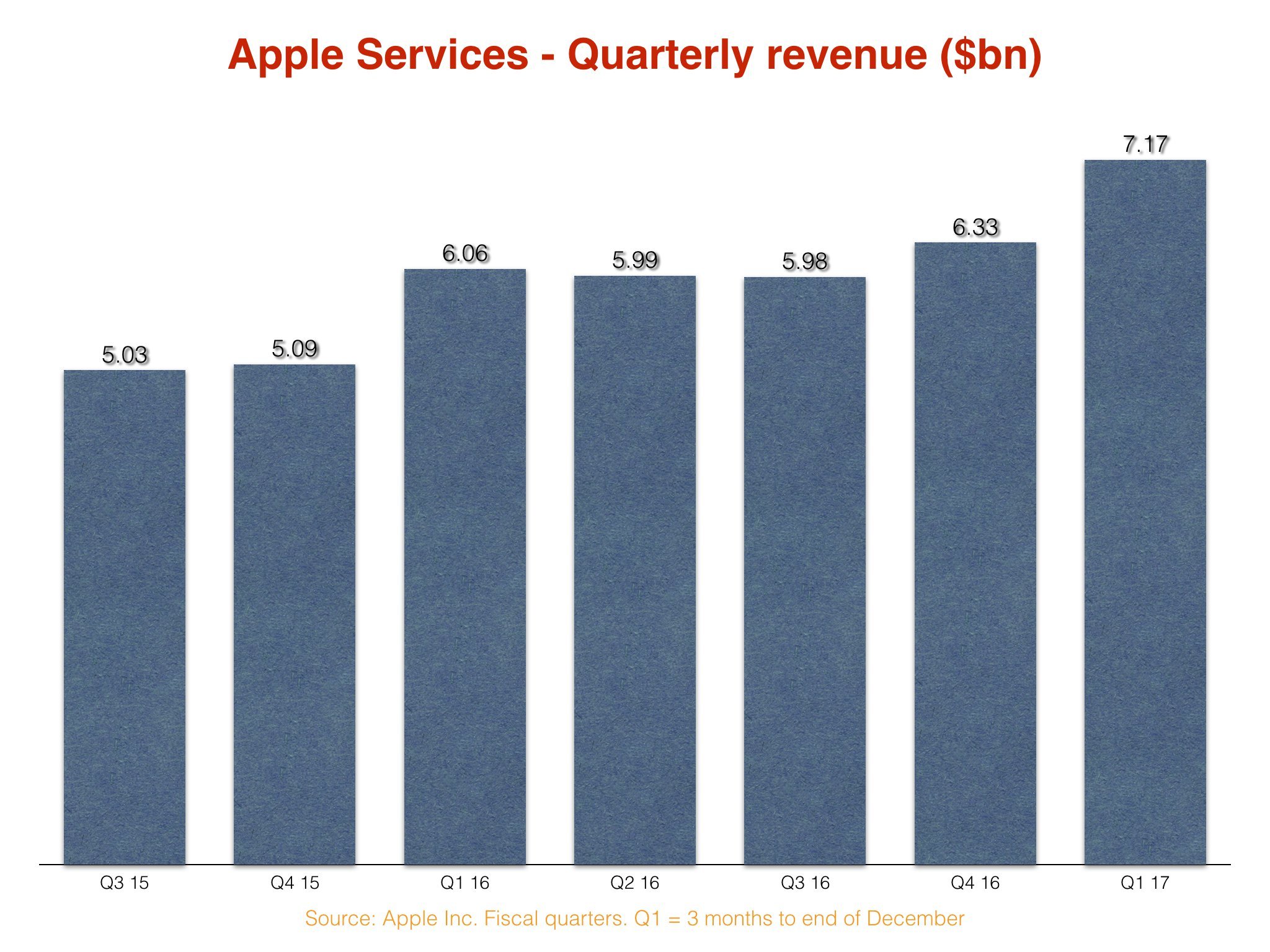

Out of the record $78.4bn Apple turned over in the three months to end of December, ‘Services’ generated $7.2bn, or just under 10%.

As growth in iPhone sales starts to slow (+5% in Q1), Apple’s focus is gradually shifting towards Services – and it’s thinking big.

After announcing an 18% year-on-year growth in Services revenue, Tim Cook told investors that “our goal is to double the size of our Services business in the next four years”.

That would mean taking the $23.8bn generated by Apple Music et al in FY2016 and growing it close to $50bn by the end of FY2020.

By the end of 2016, according to MIDiA Research, the Spotify competitor had attracted 20.9m subscribers to its platform.

Although student/family promotions, telco bundles and territorial differences will bring down the average revenue of these subs below the standard $9.99-a-month Apple Music pricetag, we can guess than in the final three months of last year, Apple Music generated somewhere close to $600m.

That’s less than 10% of Apple’s total Services revenues in the period – dwarfed by the App Store, which generated $3bn in December alone.

But to consider Apple Music an also-ran in terms of its parent’s new Services focus would be a mistake.

It may yet prove to be the jewel in the crown.

For one thing, Apple Music is a subscription platform. And Apple is falling stone in love with subscription right now.

“Our Services offerings are driving over 150 million paid customer subscriptions,” Cook told investors, proudly.

“This includes our own services, and third-party content that we offer on our stores.”

He clarified that Apple “participates economically” from these third-party products – a reference to the fact that Apple hoovers up a percentage of App Store subscription cash from the likes of Spotify, in what opponents disparagingly refer to as the ‘App Tax’.

Apple Music, on the other hand, is a first-party cash generator, bringing its parent a much fatter margin than these non-Apple competitors.

It’s the strategic test-bed for an original content strategy; one which Cook hopes will turbocharge Services’ growth over the next half-decade – and which may consequently draw a bountiful chunk of that $246bn from his grasp.

“we have put our toe in the water doing some original content for Apple Music, and that will be rolling out through the year.”

Tim Cook

“In terms of original content, we have put our toe in the water with doing some original content for Apple Music, and that will be rolling out through the year,” said Cook, in response to a direct question over whether Apple could use its massive cash reserves to buy more entertainment copyrights.

“We are learning from that, and we’ll go from there.”

Cook added: “Obviously, with our toe in the water, we’re learning a lot about the original content business and thinking about ways that we could play at it.”

MBW hears from very senior sources that last year, Apple directly offered to match one pop superstar’s major label advance if he spurned a traditional record company deal, and instead committed his new album exclusively to Apple’s platforms.

Perhaps wisely, he stuck with convention and said no.

Meanwhile, people tend to forget that Vivendi swatted away an $8.5bn acquisition offer for Universal Music Group from SoftBank in 2013 – before Credit Suisse valued the company at €10bn a year later.

For the record, that figure amounts to just 5% of Apple’s current cash haul.

We’re not saying that Tim Cook will definitely be looking at major-scale music copyright as an acquisition target.

But when you’ve got more than $200bn lying around, ‘playing at it’ tends to mean something drastically different than it does even to the music industry’s established giants.

Interesting times ahead.