Revenue growth in the USA’s recorded music market accelerated last year, with overall industry sales increasing by $1.2bn.

In 2016, the market increased by close to half that amount – $787m.

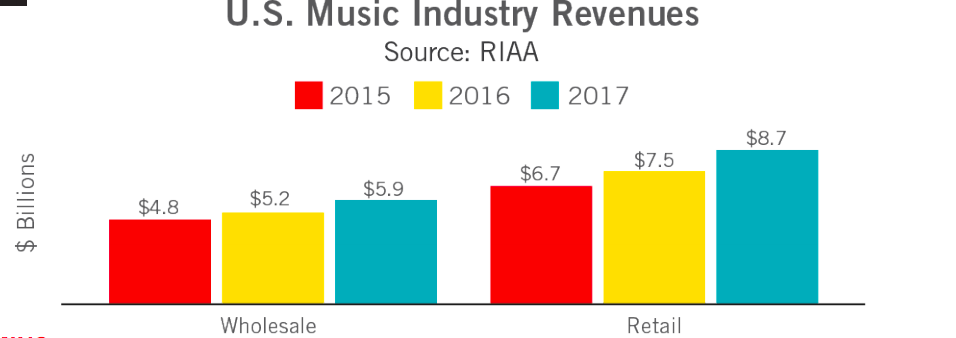

The US market brought in $8.72bn in total in 2017 across all formats, according to new RIAA stats, up 16.5% (or $1.23bn) year-on-year on a retail basis.

And on a wholesale basis – ie. the money flowing through to labels and artists – revenues increased 12.6% (or $700m) to $5.9bn.

(It’s interesting to consider how new label deals with Spotify signed last year – at a lower margin than previous agreements – affected the clear difference between these retail and wholesale % growth figures.)

The $8.7bn retail revenue sum is the same level the industry was at a decade ago, in 2008. It remains 40% below peak levels, not accounting for inflation.

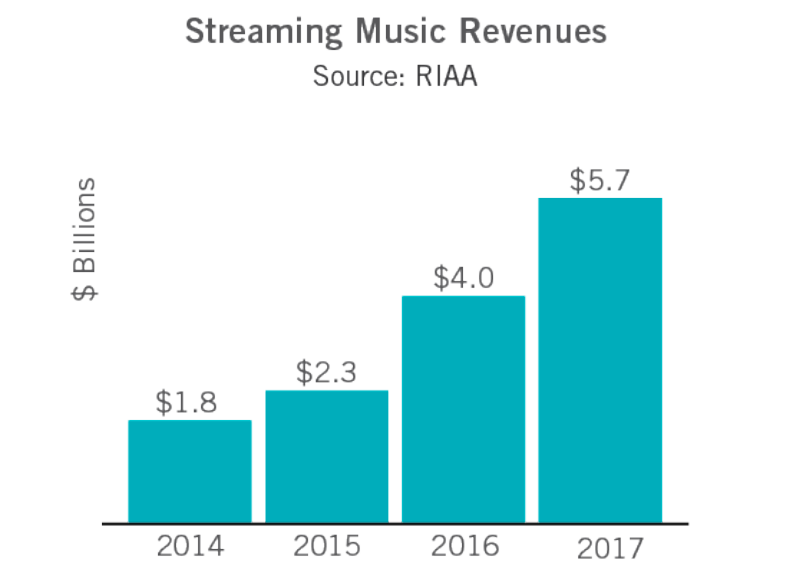

The driving force behind this growth was – of course – streaming services, which saw their US retail revenues grow by 43% to $5.7bn last year.

That was enough to claim 65% of the overall US recorded music market.

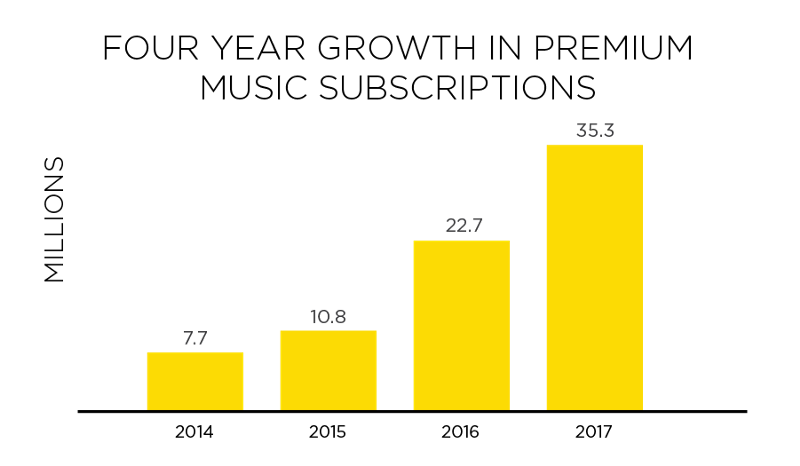

The number of paying streaming subscribers to ‘full’ premium on-demand services hit 35.3m in the year on average – up by 56%, or 12.6m people, on the 22.7m monitored in 2016.

This was a bigger jump in subscribers than that seen in 2017, when paid subscriptions moved up by 11.9m.

(To put 35m into context: that’s close to the entire population of Canada.)

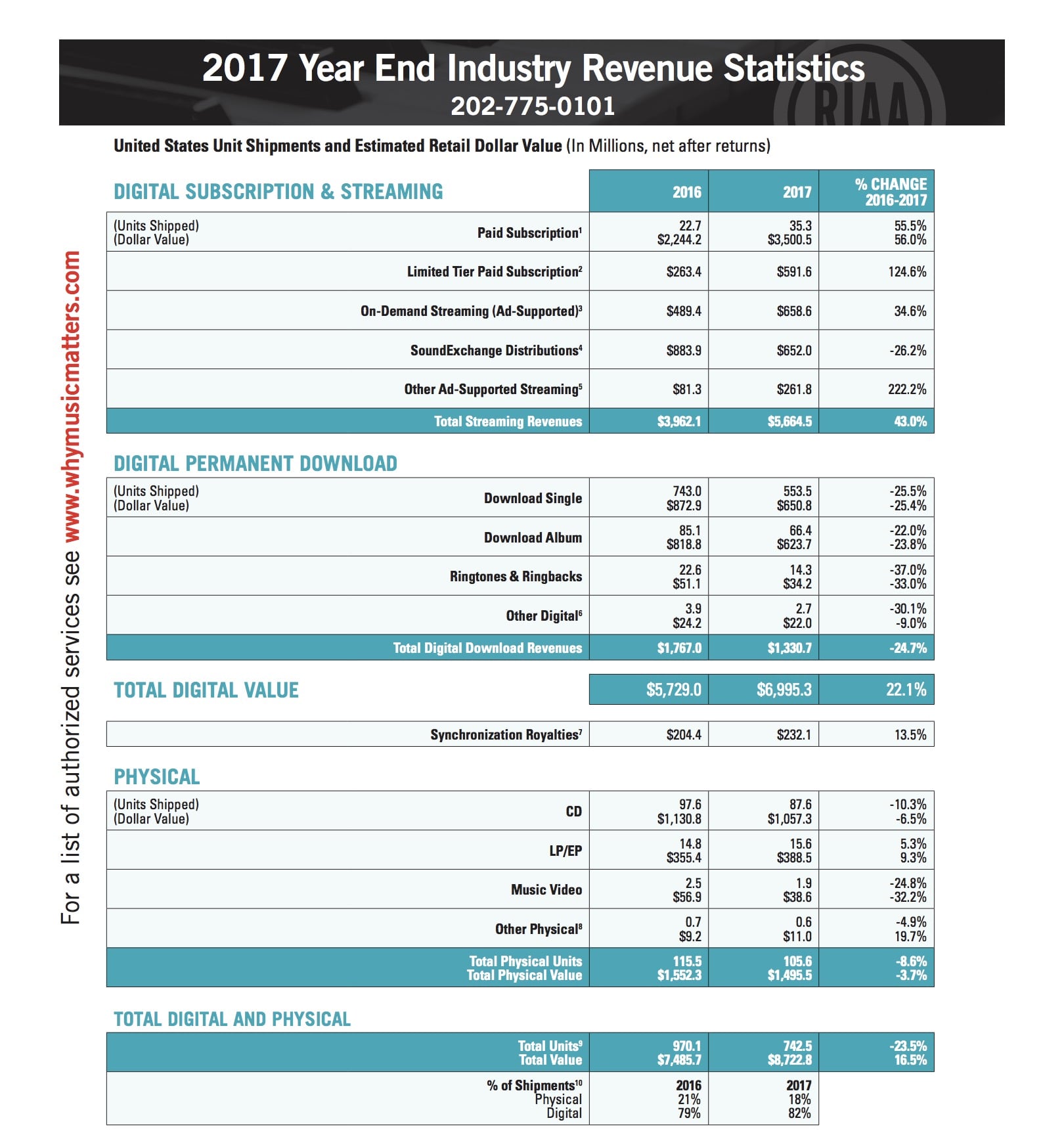

Because of this growth, paid streaming subscriptions to ‘full’ premium services like Apple Music and Spotify Premium generated $3.5bn in 2017, up 56% year-on-year.

In addition, “limited tier” subscription services – like Amazon Prime and Pandora Plus – generated $591.6m last year, up 124.6% YoY.

Combined, these streaming subscription categories generated more than $4bn in the 12 months.

Ad-supported interactive streaming services like YouTube and Spotify’s free tier saw revenues grow 34.6% to $658.6m, while digital radio services – whose royalties are collected by SoundExchange – generated $652m, down 26% year-on-year.

(As previously explained, this is largely because Pandora now has direct deals with labels, meaning its royalty payouts no longer register in SoundExchange’s numbers.)

Total digital download revenues fell by 24.7% to $1.3bn, with the money generated by digital albums tumbling 23.8% to $623.7m.

Retail sales of CDs dipped by 6.5% to $1.06bn, while largely thanks to another spirited year for vinyl albums – up 9.3% to $389m – total physical revenues fell by just 3.7% to $1.5bn.

Recorded music sync royalties had a banner year, rising by 13.5% to $232.1m.

RIAA chief Cary Sherman was upbeat about the results today – but offered a note of circumspection over the future prospects of the industry, pointing out his concern regarding a “distorted market”.

He said: “We‘re delighted by the progress so far, but to put the numbers in context, these two years of growth only return the business to 60% of its peak size — about where it stood ten years ago — and that’s ignoring inflation. And make no mistake, there’s still much work to be done in order to make this growth sustainable for the long term.

“Growth is of course welcome, for many reasons, but especially because it will result in more investment in artists and music.

“However, we continue to operate in a distorted marketplace, replete with indefensible gaps in core rights, inhibiting investment in music and depriving recording artists and songwriters of the royalties they deserve.”

He added: “The playing field remains unfairly tilted at the expense of creators and digital music services, resulting in a ‘value gap,’ the gulf between the amount of music being consumed and the compensation that platforms return to music creators for exploiting the music. The economic consequences are real and increasingly documented by leading academics.”

You can see the full set of RIAA results below.

[Pictured: Ed Sheeran, whose Divide was Nielsen’s top album of the year in the US market.]

Music Business Worldwide