The IFPI Global Music Report 2025 reveals a music industry continuing to grow – while facing new challenges and opportunities.

To be clear: the IFPI’s numbers refer strictly to wholesale recorded music revenues (i.e. the money paid through to labels, distributors, and artists).

The worldwide numbers contain some good news for rightsholders (see: subscription streaming trade revenues up nearly 10% YoY), but there are also some worrying elements (see: ad-supported streaming not pulling its weight, a slump in the USA’s performance).

Here are 11 quick takeaways from the report, which can be downloaded, through here:

1. Continued Growth for a Tenth Year

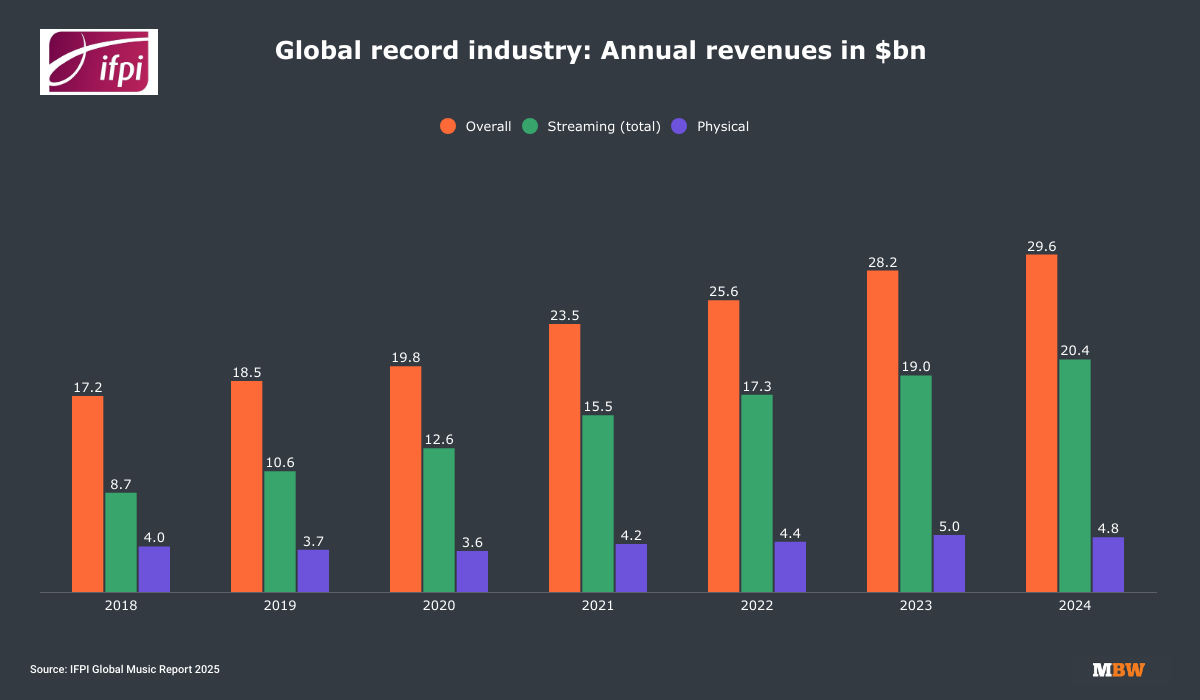

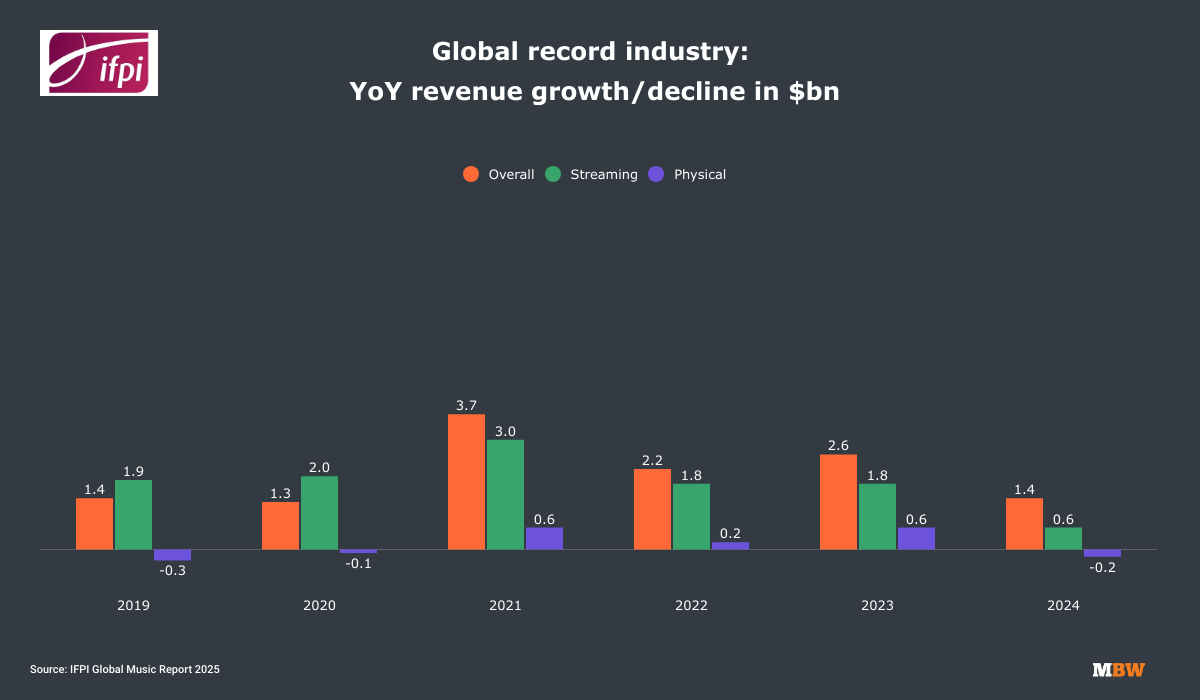

Global recorded music revenues grew 4.8% YoY in 2024, reaching USD $29.6 billion.

This marks the tenth consecutive year of growth, though the pace has slowed compared to previous years.

The IFPI previously reported that the global industry grew by 10.2% YoY in 2023, suggesting the percentage growth of the business roughly halved in 2024 vs. the prior year.

2. A strong year for some emerging markets

Three of the world’s seven regions posted YoY double-digit gains: Middle East & North Africa (MENA) led at +22.8% YoY, followed by Sub-Saharan Africa (+22.6% YoY) and Latin America (+22.5% YoY).

Sub-Saharan Africa saw revenues surpass USD $100 million for the first time (USD $110 million). These emerging regions are significantly outpacing mature markets in percentage terms.

3. Europe’s Strong Performance

Europe grew by 8.3% YoY, representing 29.5% of global revenues in 2024, maintaining its position as the second-largest region.

Europe (including the UK) added more revenue growth than any other region.

The region’s three largest markets all generated YoY revenue growth: UK (+4.9% YoY), Germany (+4.1% YoY) and France (+7.5% YoY).

4. A Disappointing Year for the USA

The United States, the world’s single largest recorded music market, posted wholesale growth of just +2.2% YoY in 2024, according to IFPI’s figures – even lower than the RIAA‘s estimate of wholesale growth in the US (+2.7% YoY) published yesterday (March 18).

Combined, the USA & Canada represented 40.3% of global revenues in 2024 after jointly growing by just 2.1% YoY.

That North American market share of global revenues is significantly down from previous years, when NA typically commanded a share closer to 45%.

The USA’s growth figure in 2024 (+2.2% YoY) were significantly below the global average growth rate of +4.8% and far behind the growth rates seen in many other regions and markets.

5. Streaming Dominance Continues

Global recorded music streaming revenues exceeded USD $20 billion for the first time (USD $20.4 billion) in 2024, representing 69.0% of total recorded music revenues.

For context, USD $20 billion was bigger than the entire recorded music industry revenues for each year between 2003-2020.

Subscription streaming was the key driver of growth, increasing 9.5% YoY, representing more than half (51.2%) of global revenues.

6. Ad-Supported Streaming Slowdown

While subscription streaming revenue increased by 9.5% YoY in 2024, ad-supported streaming formats grew by a troublingly low +1.2% YoY.

This represents a significant gap between the two streaming revenue sources, with paid subscription services driving the majority of streaming growth.

7. Physical Formats endure Mixed Results

Physical music trade revenues declined by –3.1% YoY in 2024.

However this followed a strong performance in 2023 when revenues soared by +14.5% YoY.

CD and music video revenues fell by –6.1% YoY and -15.5% YoY respectively.

In contrast, global vinyl revenues continued to grow, up 4.6% YoY, marking the format’s 18th consecutive year of growth. Physical formats represented 16.4% of total global revenues.

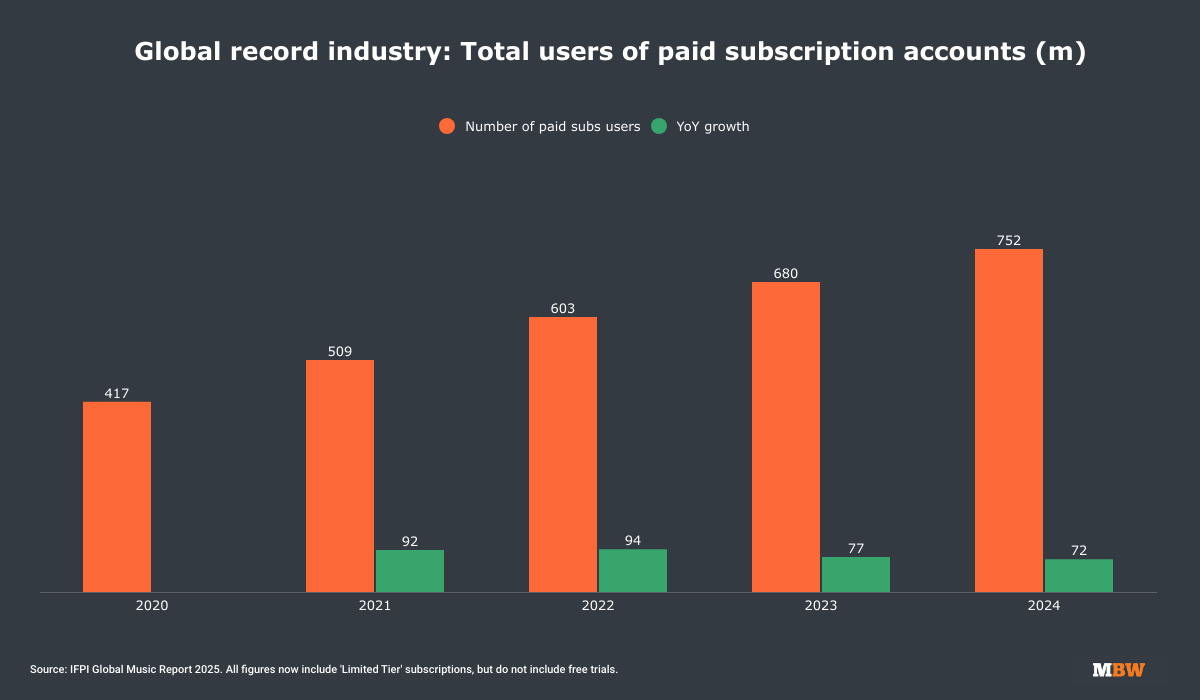

8. Subscription User Growth

The total number of users of paid music streaming subscription accounts grew 10.6% YoY to 752 million globally in 2024.

This strong growth in the subscriber base continues to drive the paid streaming segment, which remains the industry’s primary revenue source.

9. Market Ranking Changes

There was movement in the top ten markets in 2024, as Mexico overtook Australia and moved up a place to feature at No.10.

Brazil’s revenues grew by an impressive 21.7% YoY, making it the fastest-growing top-ten market, while Mexico increased revenues by 15.6% YoY.

Fifty-five out of 58 markets recorded growth in 2024, which included eight of the top 10 global markets.

10. Asian Markets post Mixed Results

Asia recorded moderate growth of +1.3% YoY in 2024, set against a strong performance in 2023 where the region grew by +14.4%.

Asia maintained its status as the world’s largest physical market and accounted for 45.1% of global physical revenues in 2024. A decline in physical sales (-4.9% YoY), therefore impacted the region’s overall growth rate.

Japan, the world’s second-largest market, was flat year-on-year (-0.2% YoY), whilst China, ranked #5 globally, increased revenues by +9.6% YoY.

11. Industry leaders seek further revenue opportunities in the years ahead

Sir Lucian Grainge, Chairman & Chief Executive Officer, Universal Music Group, emphasized that “it’s more critical than ever that we continue to advance the artist-centric principles that elevate the entire music ecosystem by rewarding real artists and those who support them.”

Rob Stringer, Chairman, Sony Music Group, added, “While we are supportive of technological change that helps bring music to fans everywhere around the world it only seems reasonable that artists be paid appropriately for their endeavours.”

Robert Kyncl, Chief Executive Officer, Warner Music Group, noted, “The future is never guaranteed – we must continue to build a collaborative environment where artists are championed, music is valued and protected, and innovation thrives.”Music Business Worldwide