MBW Views is a series of exclusive op/eds from eminent music industry people… with something to say. The following comes from Bill Werde (pictured inset), Director of the Bandier music business program at Syracuse University and a former Editorial Director of Billboard. This essay originally appeared in Full Rate No Cap, Werde’s free, weekly email of music industry analysis.

Latin music generated well-deserved headlines and analysis last week.

The RIAA released its final 2022 numbers for Latin music and showed that the genre had blown past the billion-dollar mark. These numbers confirm a couple of things that we basically already knew: one, that Latin music is a powerhouse global genre, with an ever-deepening bench of stars. And two, Bad Bunny is an absolute music industry stud.

I had some fun playing with the numbers and by my estimation, Bad Bunny probably represents about 20% of the recorded revenue of that whole genre. That’s staggering–it’s possible that no single artist has ever been responsible for a larger chunk of one genre in history.

But while I was celebrating a nice win for all of my friends in the Latin industry, I was also reminded of something that’s probably timely to bring back up: YouTube still has a value gap.

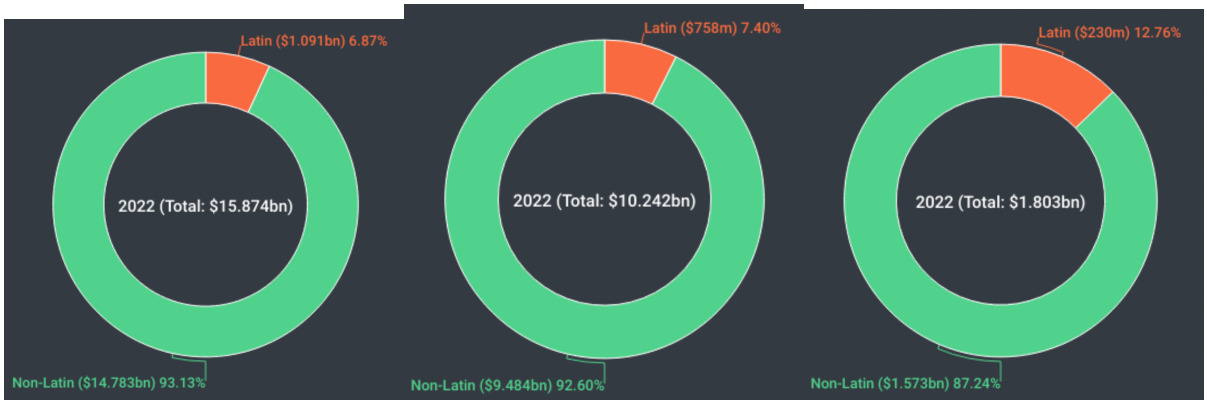

This jumped out at me while I was thinking about the great analysis and charts that Music Business Worldwide published, connected to the RIAA news.

You’ll notice that Latin music indexes much higher for free, ad-supported tiers than it does in paid subscriptions. Left to right, below, you can see Latin music’s share of the overall U.S. market; Latin music’s share of the overall U.S. streaming market; and Latin music’s share of ad-supported music streams in the U.S.

(Chart brazenly excerpted from this page of awesome MBW analysis on all things Latin music.)

It made me wonder, what would Latin music be worth if ad-supported tiers paid more? What if YouTube’s ad-supported business models were actually subjected to free market dynamics and negotiations?

Let me take a quick step back, and explain “the value gap.”

Back in 2016 and 2017, before it was abundantly clear that paid streaming subscriptions would create rapid and sustainable growth for the music industry, YouTube’s value gap was a hot topic.

There is no greater, or more political, strategic mouthpiece for the global, corporate industry than the annual IFPI report. And they used the 2017 edition to fire serious shots at YouTube:

It’s important to remember that these are based on 2016 numbers (I’ll come back to what has and hasn’t changed since). But this pretty clearly illustrates the value gap: simply put, the revenue is way way way out of whack with the usage. Ad-supported streamers (aka YouTube, primarily) generate a much larger percentage of global music consumption than their percentage of global music revenue.

Why did the labels and publishers let this happen? They really had no choice. The “safe harbor” provision of the DMCA — in short, streaming platforms have limited liability for infringement, as long as they are responsive to takedown notices — meant that they could either negotiate with YouTube on YouTube‘s terms, or they could spend inordinate, perpetual resources issuing endless takedown notices. Because safe harbor provisions only insist that platforms take down an infringing song–and not that they keep it down–labels could either take what was offered from YouTube, or effectively get nothing at all. Either way, their songs were going to be on the platform.

But an interesting thing happened in the ensuing years. YouTube became an incredibly valuable contributor to the global music business on two different levels. On one hand, as the labels became more and more interested in global expansion, YouTube was (and very much remains) an affordable and popular option for fans in many emerging markets. And in aggregate, YouTube’s global scale started to pay off: YouTube touted this themselves last year, announcing that they had contributed $6 billion to the global music industry in the previous 12 months.

No doubt, that’s a lot of money. YouTube’s 12-month period was from July 2021 through June 2022, so it doesn’t align perfectly with the IFPI’s full year 2022. But YouTube’s chunk of change represents just under 23 percent of that global IFPI recorded music revenue number. So problem solved, right? The value gap is closed?

This is where it gets tricky, and also where it becomes a little more clear that we are probably onto something important. Because YouTube, a company that shouted that $6 billion number from the mountaintops, also recently shared specific, impressive numbers about music service subscribers and the growth of TikTok competitor Shorts (50 billion daily views!).

So riddle me this: how come YouTube doesn’t trumpet their undoubtedly, staggeringly impressive volume numbers? Why no blog post trumpeting their total music streams?

I suspect the answer is because it would make it too easy to do the math showing the value gap. And I say this as someone who just spent a week trying to do the math. If those numbers were known, it would be easy to pinpoint what YouTube was paying for music, and create transparent, public industry debate about whether that’s a fair number. Instead, we are left to get data from industry analysts and surveys. But those surveys all make it pretty clear that YouTube is likely responsible for more–much, much more–than 23 percent of global music consumption. Despite YouTube’s substantial global contributions to the music industry, a value gap remains.

Let’s first tackle the global picture as best we can. Below is a snapshot of “active users who listen to music” by platform. And you can see, YouTube music appears to have almost as many active users as every other platform combined!

Now let’s look at the global revenue picture for recorded music:

Ad-supported revenue is worth only 18.7 percent of the global total. And that 18.7 percent includes plenty of other audio-only ad-supported tiers, such as Spotify‘s.

Of course, YouTube (via YouTube Music) contributes additional revenue that would be attributed to subscription audio streams in the above chart. But we know that all-in, YouTube caps out at about $6 billion. Globally, it appears that YouTube may be used for somewhere in the ballpark of half of all music consumption, but less than a quarter of recorded music revenue. Value gap.

The picture in the United States isn’t much different. We have no clear, specific public numbers. But take a look at platform use ranked by percentage of monthly U.S. music listeners. YouTube is first, with nearly double the users as the next-closest platform.

But when it comes to revenue?

As you can see in the charts below, the ad-supported category, which includes more than just YouTube, is worth $1.8B, or 13.5 percent of U.S. recorded music revenues. Likely: Value gap.

So, what would be a “fair” amount of revenue from YouTube? On one extreme, we could say that if we made the percentage of global recorded music revenue that YouTube contributed, in line with the percentage of global recorded music consumption that YouTube represents, the gains for music would be massive. This would almost certainly be a billion+ dollar boost to the global music business, and possibly much more.

Is that realistic in an age when advertising revenues have been largely flat or declining? Are there other numbers and factors to consider? Of course. But as recorded music revenue growth from paid subscriptions starts to level off globally, the major labels are basically beginning to look for proverbial spare change in the couch cushions, and trying to find new, substantial revenue streams. Should the majors be re-examining YouTube’s payouts in this context? Probably.

Absolutely none of this is meant to vilify YouTube. I want to be very clear about that. YouTube is a critical partner for the music industry, and any negotiations would obviously must be done with respect to this. But as the music industry enters a phase where 20% year-over-year subscription growth can no longer be assumed, is it fair to put a little more squeeze on YouTube? Should rights holders still be agitating to reform safe harbor provisions?

Yes and yes. If nothing else, it is fun to think about what Bad Bunny would be worth if YouTube streams paid just a little more.Music Business Worldwide