Image credit: NetflixThe most-viewed title on Netflix in H2 2024 was 'Squid Game - Series 2', with 619.9 million hours of consumption

Speak to pretty much any senior figure at the world’s largest music rightsholders, and you’ll find it’s a bone of contention for them all.

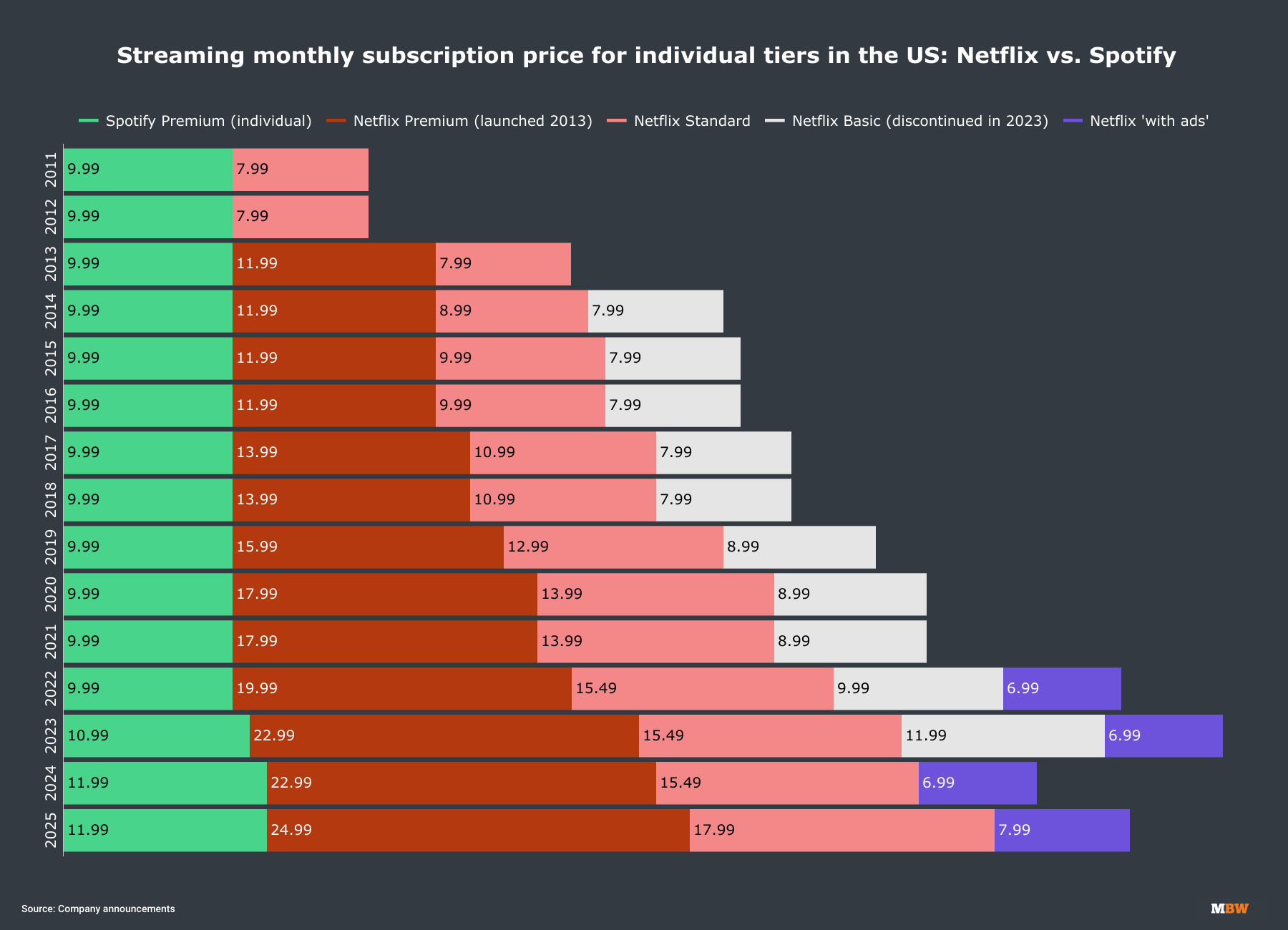

How come a standard music streaming subscription in the US costs USD$11.99 per month, when – over in the land of film and TV – Netflix charges $17.99 per month for its equivalent service?

The answer, of course, is the consistency of Netflix’s price hikes over the past decade.

As recently as 2016, an individual subscription to Netflix’s Standard tier in the States cost consumers exactly the same amount per month ($9.99) as an Individual Premium sub to Spotify.

In the nine years since, Netflix has increased the US price of its Standard tier five times, most recently at the start of 2025.

During the same time span, Spotify has increased its US individual Premium price just twice (in 2023, and then again in 2024).

Many argue that it’s illogical for a service like Spotify, offering listeners unlimited access to almost every record ever made, to be priced significantly lower than Netflix, which offers access to a limited array of TV titles and movies.

Others point out that Spotify’s pricing model, born out of the dark days of piracy, complicates matters. The firm’s freemium ‘funnel’ is based on attracting users to its ad-supported ‘free’ tier and then, later, converting these free users into paying customers.

Netflix, by contrast, remains a pay-only service, although it did introduce a lower-priced, ad-supported tier in 2022.

The background: A shock to the system

After a decade of hockey stick growth, music streaming’s revenue trajectory, especially from a rightsholder perspective, has significantly decelerated over the past year.

That’s particularly true in the world’s largest music market, the United States.

Witness last week’s IFPI results, which mapped out the latest annual global trade revenues of the worldwide recorded music industry.

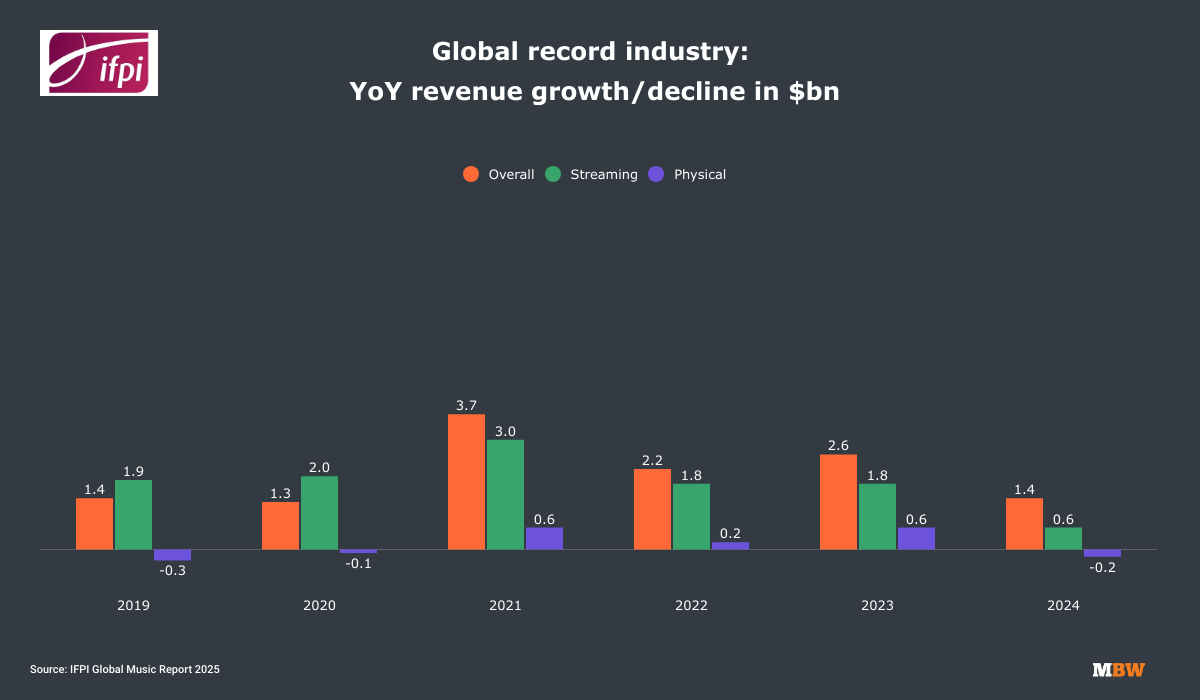

In the US, overall recorded music trade revenues grew by just 2.2% YoY in 2024, less than the market’s rate of inflation in the same 12 months.

Perhaps more worrying was the fact that worldwide trade revenues from ad-supported music streaming platforms (like YouTube and Spotify ‘free’) grew by just 1.2% YoY last year.

Based on latest retrospective IFPI data; ‘streaming’ includes subscription and free services, audio plus video

The IFPI‘s report did contain some brighter news for rightsholders and their investors, however.

The global trade revenue generated by subscription (i.e. paid-for) streaming in 2024 was up 9.5% YoY, growing by an estimated +$1.4 billionYoY (to $15.2 billion).

According to MBW’s calculations, that was a slightly larger annual jump in global subscription revenues than that recorded in both 2023 and 2022, which each saw increases of ~$1.3 billion (based on the latest IFPI stats).

Meanwhile, in other positive news for rightsholders yearning for bigger returns, Spotify is reported to be readying a ‘Music Pro’ tier later this year, priced at $5.99 per month more than its standard Premium tier (i.e., around $18 pm). Music Pro may offer AI-assisted remix capabilities, hi-def audio, and better ticketing integration.

Rightsholders say they are optimistic about the impact launches of ‘superfan’ tiers like ‘Music Pro’ will have on the value they see from the market.

Robert Kyncl, CEO of Warner Music Group, indicated earlier this month that his company’s latest deals with Spotify and Amazon Music had brought WMG some “certainties” regarding plannedprice elevation at the services in the months and years ahead.

Average Revenue per Content hour: A new way

So, to recap: Netflix’s standard tier is at a much higher price point than Spotify’s equivalent, while concerns are growing over the commercial returns the music biz is seeing from (a) ad-supported streaming and (b) the United States as a market more generally.

A pertinent question, then: Is it time for the music business to start considering its core product less in terms of price and more in terms of value for money?

What if we stopped obsessing over monthly subscription prices and started measuring something more illuminating: how much revenue each hour of consumed content generates?

This metric — Average Revenue Per Content Hour (ARPCH) — offers the music business a wake-up call and a powerful new lens through which to evaluate its fundamental worth.

To help, let’s bring Netflix’s business back into focus.

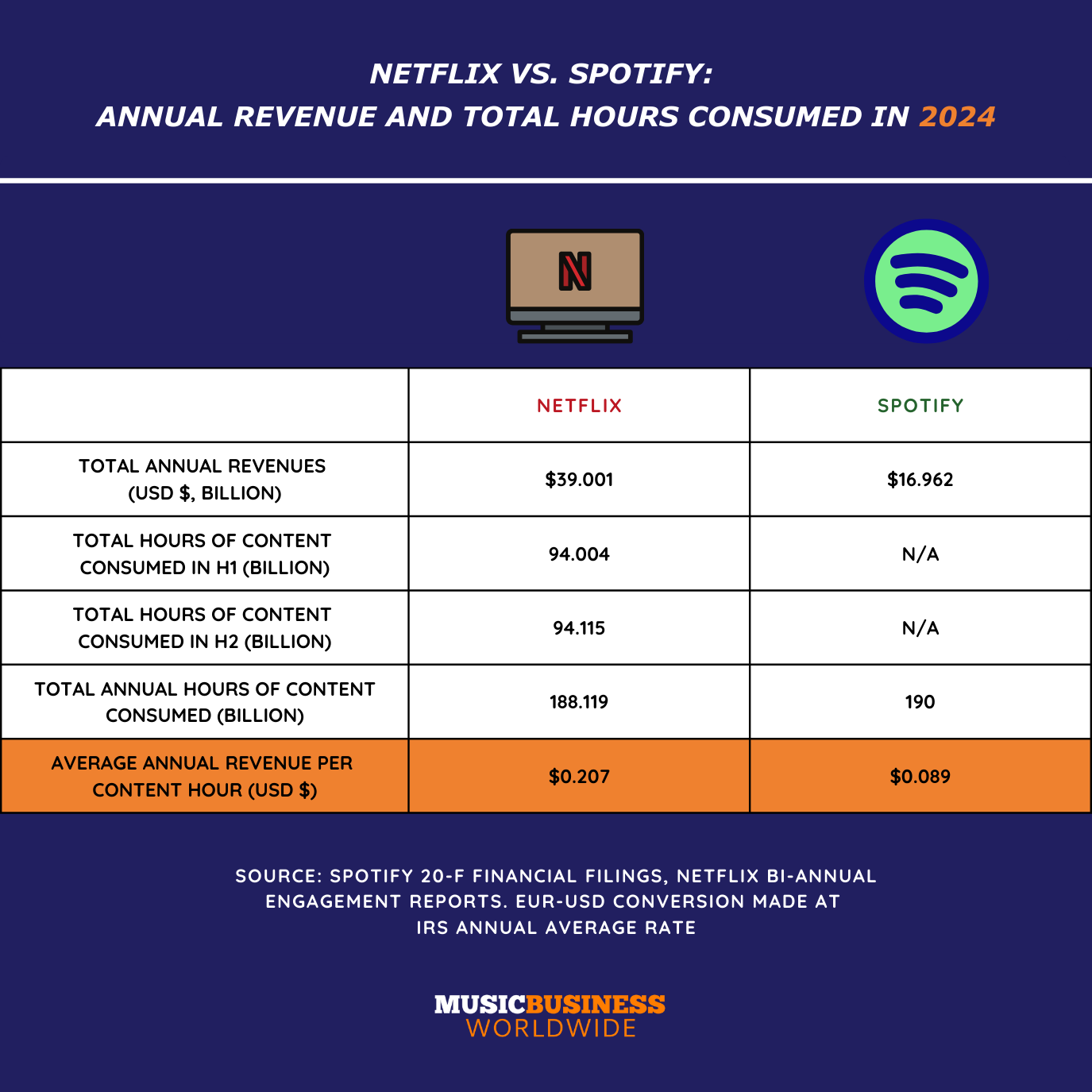

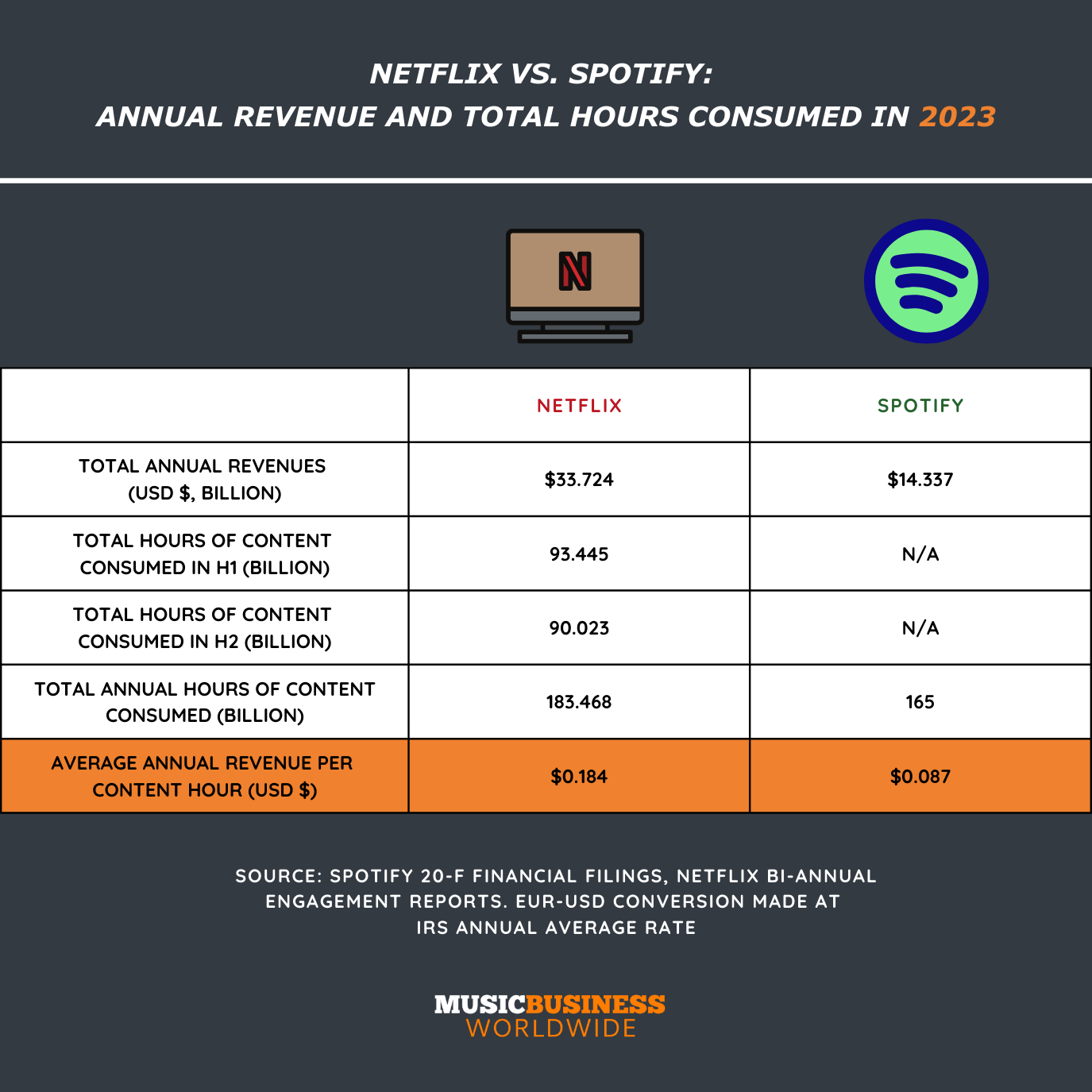

Over the past two years, Netflix has revealed, via its bi-annual Engagement report, the total number of consumption hours its content has attracted.

These figures cover ~99% of Netflix consumption, taking into account only the TV shows/movies that have surpassed a minimum watch-time threshold.

MBW has run the numbers in the data spreadsheets pushed out by Netflix and calculated the total number of hours ‘watched’ globally on the platform in 2023 and 2024.

Meanwhile, Spotify’s annual 20-F report also estimates the total number of hours of content consumed (i.e., total cumulative play-time) by its users each year.

Interestingly, Netflix and Spotify’s numbers are strangely similar.

For example, in 2024, Netflix users consumed 188.1 billion hours of content, whileSpotify’s users racked up 190 billion hours.

Using this data and the total annual revenue reported by each service, we’ve calculated the Average Revenue Per Content Hour (ARPCH) figure across each platform.

As you can see below, in 2024, Netflix generated USD $0.207 per hour of content consumed (ARPCH) by each customer.

Spotify, meanwhile, generated less than half this amount, at $0.089 per hour.

Spotify’s ARPCH didn’t greatly change from 2023 to 2024 ($0.089 vs. $0.087), despite a headline-grabbing price rise at the service last summer (when its US flagship tier moved from $10.99 per month to $11.99 per month).

Netflix, however, did see a significant annual rise in its ARPCH in 2024, up from $0.184 in 2023 to $0.207 the following year.

Once again, in 2023, Netflix’s ARPCH was more than double the size of Spotify’s ($0.184 vs. $0.087), but the gulf between the two widened in 2024.

Conclusions – and a bigger question?

There are, however, obvious key differences between Spotify and Netflix’s business models and reach.

At the close of 2024, Netflixhad 301.6 million paying ‘members’; Spotify had 263 million users of paid subscription accounts but 675 million total users (including paid and ‘free’ users).

Yet despite this, the two companies have a similar global footprint: Netflix is available in over 190 countries (not including China), while Spotify is available in over 180 markets (not including China).

In the music business, we often compare and contrast the pricing structure of our streaming services with that of film and TV and ponder how such a gulf in monthly account costs has developed.

Looking at Average Revenue Per Content Hour (ARPCH) offers a fresh angle, sharpening our focus on a more essential question: how much is 60 minutes’ access to the entire world of music worth vs. 60 minutes’ access to a limited spread of premium film and TV content?

Is it really justifiable, from a music rightsholder perspective, that Spotify’s ARPCH is less than half the size of Netflix’s – and losing ground?

If not, what can be done about it? Should Spotify, in addition to launching ‘Music Pro’ push the price of its standard streaming subscription much higher, especially in the US?

“As Sony‘s Rob Stringer has previously suggested, should we be questioning whether Spotify ‘free’ users – in the US, especially – could now be asked to pay a low price (vs. nothing at all) for access to ad-supported streaming?”

And what of SPOT’s ‘free’ tier – a major factor in its ARPCH lagging behind Netflix?

Has the time now come for a reduction in the content available on Spotify’s ad-funded offering in larger markets?

Or, as Sony’s Rob Stringer has previously suggested, should we be questioning whether Spotify ‘free’ users – in the US especially – could now be asked to pay a low monthly price (vs. nothing at all) for access to ad-supported streaming?

Doing so would bring Spotify’s ad-supported tier closer to the model of Netflix’s own equivalent. (A subscription to Netflix’s ‘Standard With Ads’ tier currently costs $7.99 per month in the United States.)

Thinking further about ARPCH and its connotations, here’s a wild suggestion: might the music biz one day consider limiting the hours of unlimited music that each consumer can enjoy on Spotifyet al before being asked to pay for more?

“You’ve used up your allotted 25 hours of unlimited music this month… please pay $X for more”.

Such a move, akin to the cloud storage pricing model seen from giants like Google (you’ve used up 50GB, please pay $X for more), might not prove popular with music fans. But it would very likely drive up the hottest new metric in town – ARPCH.

Notes: You can download the full spreadsheet reports of Netflix’s engagement reports (‘What We Watched’) at the following links: H1 2023; H2 2023; H1 2024; H2 2024.

As annotated, Spotify’s annual total revenues in 2024 (EUR €15.673bn) and 2023 (EUR €13.247bn) have been converted to USD at the IRS’s average annual rate.Music Business Worldwide